Grease Trap V1.0The Grease Trap V1.0 indicator is a dynamic, Fibonacci-based strategy that calculates unique moving averages to generate trading signals. Below is an overview of its main components and functionality:

How It Works

Fibonacci Grouped Averages:

Dynamic Fibonacci Sequence:

The indicator uses a custom function that dynamically builds a Fibonacci sequence. The user can set the number of Fibonacci elements for two separate calculations:

One for the Indicator Average (default: 9 elements).

One for the Base Average (default: 14 elements).

Grouped Averaging:

Using these Fibonacci numbers, the script groups historical closing prices into segments. For each group (with a length determined by a Fibonacci number), it computes an average. These individual group averages are then averaged together to produce a single dynamic average.

Plotting and Visual Cues:

Two Lines:

The indicator plots two lines on the chart:

Primary Dynamic Fibonacci Grouped Average

Base Dynamic Fibonacci Grouped Average

Color Coding:

The colors of these lines change based on their relationship to the current high price and to each other. For example, if the primary average is above the high or crosses above the base average, it might be shown in green or yellow, whereas certain conditions trigger red, signaling caution.

Crossover Dots:

When the primary average crosses above the base (a bullish signal), a green dot is plotted. Conversely, when it crosses below (a bearish signal), a red dot is displayed. These dots help visually pinpoint the moments of potential trade entry or exit.

Trading Signals and Orders:

Buy Signal:

Triggered when the primary average crosses above the base average. On a buy signal:

If in a short position, it closes that position.

Then, it enters a long position.

Sell Signal:

Triggered when the primary average crosses below the base average. On a sell signal:

If in a long position, it closes that position.

Then, it enters a short position.

Profit Target Management:

The indicator includes automated profit management:

For long positions, it sets an exit order when the price rises by a user-defined percentage (default: 2%).

For short positions, it sets an exit order when the price falls by a similar percentage.

Alerts:

The script is equipped with alert conditions. Traders receive notifications whenever a buy or sell signal is generated, helping them stay on top of potential trading opportunities.

Customization

User Inputs:

Traders can adjust:

The number of Fibonacci elements for each average calculation.

Profit target percentages for both long and short positions.

Data Length Requirement:

The script ensures it uses at least 200 data points (or the total number of available bars, whichever is greater) for a robust calculation of the averages.

In Summary

The Grease Trap V1.0 indicator combines the mathematical elegance of Fibonacci sequences with dynamic grouped averaging. It offers:

Innovative Moving Averages: Based on Fibonacci groupings of historical price data.

Clear Visual Cues: Through color-coded lines and crossover dots.

Automated Trading Actions: With built-in order management and profit targets.

Alert Notifications: So traders are instantly aware of key market signals.

This makes the Grease Trap V1.0 a comprehensive tool for both signal generation and automated strategy execution, suitable for traders looking to integrate Fibonacci principles into their trading systems.

Cerca negli script per "the script"

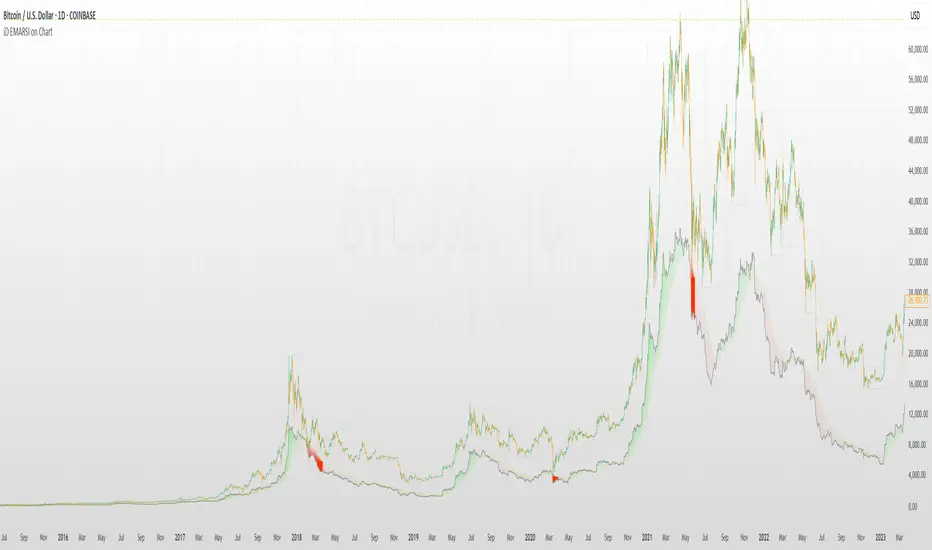

iD EMARSI on ChartSCRIPT OVERVIEW

The EMARSI indicator is an advanced technical analysis tool that maps RSI values directly onto price charts. With adaptive scaling capabilities, it provides a unique visualization of momentum that flows naturally with price action, making it particularly valuable for FOREX and low-priced securities trading.

KEY FEATURES

1 PRICE MAPPED RSI VISUALIZATION

Unlike traditional RSI that displays in a separate window, EMARSI plots the RSI directly on the price chart, creating a flowing line that identifies momentum shifts within the context of price action:

// Map RSI to price chart with better scaling

mappedRsi = useAdaptiveScaling ?

median + ((rsi - 50) / 50 * (pQH - pQL) / 2 * math.min(1.0, 1/scalingFactor)) :

down == pQL ? pQH : up == pQL ? pQL : median - (median / (1 + up / down))

2 ADAPTIVE SCALING SYSTEM

The script features an intelligent scaling system that automatically adjusts to different market conditions and price levels:

// Calculate adaptive scaling factor based on selected method

scalingFactor = if scalingMethod == "ATR-Based"

math.min(maxScalingFactor, math.max(1.0, minTickSize / (atrValue/avgPrice)))

else if scalingMethod == "Price-Based"

math.min(maxScalingFactor, math.max(1.0, math.sqrt(100 / math.max(avgPrice, 0.01))))

else // Volume-Based

math.min(maxScalingFactor, math.max(1.0, math.sqrt(1000000 / math.max(volume, 100))))

3 MODIFIED RSI CALCULATION

EMARSI uses a specially formulated RSI calculation that works with an adaptive base value to maintain consistency across different price ranges:

// Adaptive RSI Base based on price levels to improve flow

adaptiveRsiBase = useAdaptiveScaling ? rsiBase * scalingFactor : rsiBase

// Calculate RSI components with adaptivity

up = ta.rma(math.max(ta.change(rsiSourceInput), adaptiveRsiBase), emaSlowLength)

down = ta.rma(-math.min(ta.change(rsiSourceInput), adaptiveRsiBase), rsiLengthInput)

// Improved RSI calculation with value constraint

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

4 MOVING AVERAGE CROSSOVER SYSTEM

The indicator creates a smooth moving average of the RSI line, enabling a crossover system that generates trading signals:

// Calculate MA of mapped RSI

rsiMA = ma(mappedRsi, emaSlowLength, maTypeInput)

// Strategy entries

if ta.crossover(mappedRsi, rsiMA)

strategy.entry("RSI Long", strategy.long)

if ta.crossunder(mappedRsi, rsiMA)

strategy.entry("RSI Short", strategy.short)

5 VISUAL REFERENCE FRAMEWORK

The script includes visual guides that help interpret the RSI movement within the context of recent price action:

// Calculate pivot high and low

pQH = ta.highest(high, hlLen)

pQL = ta.lowest(low, hlLen)

median = (pQH + pQL) / 2

// Plotting

plot(pQH, "Pivot High", color=color.rgb(82, 228, 102, 90))

plot(pQL, "Pivot Low", color=color.rgb(231, 65, 65, 90))

med = plot(median, style=plot.style_steplinebr, linewidth=1, color=color.rgb(238, 101, 59, 90))

6 DYNAMIC COLOR SYSTEM

The indicator uses color fills to clearly visualize the relationship between the RSI and its moving average:

// Color fills based on RSI vs MA

colUp = mappedRsi > rsiMA ? input.color(color.rgb(128, 255, 0), '', group= 'RSI > EMA', inline= 'up') :

input.color(color.rgb(240, 9, 9, 95), '', group= 'RSI < EMA', inline= 'dn')

colDn = mappedRsi > rsiMA ? input.color(color.rgb(0, 230, 35, 95), '', group= 'RSI > EMA', inline= 'up') :

input.color(color.rgb(255, 47, 0), '', group= 'RSI < EMA', inline= 'dn')

fill(rsiPlot, emarsi, mappedRsi > rsiMA ? pQH : rsiMA, mappedRsi > rsiMA ? rsiMA : pQL, colUp, colDn)

7 REAL TIME PARAMETER MONITORING

A transparent information panel provides real-time feedback on the adaptive parameters being applied:

// Information display

var table infoPanel = table.new(position.top_right, 2, 3, bgcolor=color.rgb(0, 0, 0, 80))

if barstate.islast

table.cell(infoPanel, 0, 0, "Current Scaling Factor", text_color=color.white)

table.cell(infoPanel, 1, 0, str.tostring(scalingFactor, "#.###"), text_color=color.white)

table.cell(infoPanel, 0, 1, "Adaptive RSI Base", text_color=color.white)

table.cell(infoPanel, 1, 1, str.tostring(adaptiveRsiBase, "#.####"), text_color=color.white)

BENEFITS FOR TRADERS

INTUITIVE MOMENTUM VISUALIZATION

By mapping RSI directly onto the price chart, traders can immediately see the relationship between momentum and price without switching between different indicator windows.

ADAPTIVE TO ANY MARKET CONDITION

The three scaling methods (ATR-Based, Price-Based, and Volume-Based) ensure the indicator performs consistently across different market conditions, volatility regimes, and price levels.

PREVENTS EXTREME VALUES

The adaptive scaling system prevents the RSI from generating extreme values that exceed chart boundaries when trading low-priced securities or during high volatility periods.

CLEAR TRADING SIGNALS

The RSI and moving average crossover system provides clear entry signals that are visually reinforced through color changes, making it easy to identify potential trading opportunities.

SUITABLE FOR MULTIPLE TIMEFRAMES

The indicator works effectively across multiple timeframes, from intraday to daily charts, making it versatile for different trading styles and strategies.

TRANSPARENT PARAMETER ADJUSTMENT

The information panel provides real-time feedback on how the adaptive system is adjusting to current market conditions, helping traders understand why the indicator is behaving as it is.

CUSTOMIZABLE VISUALIZATION

Multiple visualization options including Bollinger Bands, different moving average types, and customizable colors allow traders to adapt the indicator to their personal preferences.

CONCLUSION

The EMARSI indicator represents a significant advancement in RSI visualization by directly mapping momentum onto price charts with adaptive scaling. This approach makes momentum shifts more intuitive to identify and helps prevent the scaling issues that commonly affect RSI-based indicators when applied to low-priced securities or volatile markets.

Strategy SuperTrend SDI WebhookThis Pine Script™ strategy is designed for automated trading in TradingView. It combines the SuperTrend indicator and Smoothed Directional Indicator (SDI) to generate buy and sell signals, with additional risk management features like stop loss, take profit, and trailing stop. The script also includes settings for leverage trading, equity-based position sizing, and webhook integration.

Key Features

1. Date-based Trade Execution

The strategy is active only between the start and end dates set by the user.

times ensures that trades occur only within this predefined time range.

2. Position Sizing and Leverage

Uses leverage trading to adjust position size dynamically based on initial equity.

The user can set leverage (leverage) and percentage of equity (usdprcnt).

The position size is calculated dynamically (initial_capital) based on account performance.

3. Take Profit, Stop Loss, and Trailing Stop

Take Profit (tp): Defines the target profit percentage.

Stop Loss (sl): Defines the maximum allowable loss per trade.

Trailing Stop (tr): Adjusts dynamically based on trade performance to lock in profits.

4. SuperTrend Indicator

SuperTrend (ta.supertrend) is used to determine the market trend.

If the price is above the SuperTrend line, it indicates an uptrend (bullish).

If the price is below the SuperTrend line, it signals a downtrend (bearish).

Plots visual indicators (green/red lines and circles) to show trend changes.

5. Smoothed Directional Indicator (SDI)

SDI helps to identify trend strength and momentum.

It calculates +DI (bullish strength) and -DI (bearish strength).

If +DI is higher than -DI, the market is considered bullish.

If -DI is higher than +DI, the market is considered bearish.

The background color changes based on the SDI signal.

6. Buy & Sell Conditions

Long Entry (Buy) Conditions:

SDI confirms an uptrend (+DI > -DI).

SuperTrend confirms an uptrend (price crosses above the SuperTrend line).

Short Entry (Sell) Conditions:

SDI confirms a downtrend (+DI < -DI).

SuperTrend confirms a downtrend (price crosses below the SuperTrend line).

Optionally, trades can be filtered using crossovers (occrs option).

7. Trade Execution and Exits

Market entries:

Long (strategy.entry("Long")) when conditions match.

Short (strategy.entry("Short")) when bearish conditions are met.

Trade exits:

Uses predefined take profit, stop loss, and trailing stop levels.

Positions are closed if the strategy is out of the valid time range.

Usage

Automated Trading Strategy:

Can be integrated with webhooks for automated execution on supported trading platforms.

Trend-Following Strategy:

Uses SuperTrend & SDI to identify trend direction and strength.

Risk-Managed Leverage Trading:

Supports position sizing, stop losses, and trailing stops.

Backtesting & Optimization:

Can be used for historical performance analysis before deploying live.

Conclusion

This strategy is suitable for traders who want to automate their trading using SuperTrend and SDI indicators. It incorporates risk management tools like stop loss, take profit, and trailing stop, making it adaptable for leverage trading. Traders can customize settings, conduct backtests, and integrate it with webhooks for real-time trade execution. 🚀

Important Note:

This script is provided for educational and template purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

Ultimate T3 Fibonacci for BTC Scalping. Look at backtest report!Hey Everyone!

I created another script to add to my growing library of strategies and indicators that I use for automated crypto trading! This strategy is for BITCOIN on the 30 minute chart since I designed it to be a scalping strategy. I calculated for trading fees, and use a small amount of capital in the backtest report. But feel free to modify the capital and how much per order to see how it changes the results:)

It is called the "Ultimate T3 Fibonacci Indicator by NHBprod" that computes and displays two T3-based moving averages derived from price data. The t3_function calculates the Tilson T3 indicator by applying a series of exponential moving averages to a combined price metric and then blending these results with specific coefficients derived from an input factor.

The script accepts several user inputs that toggle the use of the T3 filter, select the buy signal method, and set parameters like lengths and volume factors for two variations of the T3 calculation. Two T3 lines, T3 and T32, are computed with different parameters, and their colors change dynamically (green/red for T3 and blue/purple for T32) based on whether the lines are trending upward or downward. Depending on the selected signal method, the script generates buy signals either when T32 crosses over T3 or when the closing price is above T3, and similarly, sell signals are generated on the respective conditions for crossing under or closing below. Finally, the indicator plots the T3 lines on the chart, adds visual buy/sell markers, and sets alert conditions to notify users when the respective trading signals occur.

The user has the ability to tune the parameters using TP/SL, date timerames for analyses, and the actual parameters of the T3 function including the buy/sell signal! Lastly, the user has the option of trading this long, short, or both!

Let me know your thoughts and check out the backtest report!

Harmony Signal Flow By ArunThis Pine Script strategy, titled "Harmony Signal Flow By Arun," uses the Relative Strength Index (RSI) indicator to generate buy and sell signals based on custom thresholds. The script incorporates stop-loss and target management and restricts new trades until the previous position closes. Here's a detailed description:

Custom RSI Metric:

The strategy calculates a 5-period RSI based on the closing price, aiming for a more responsive measure of price momentum.

RSI thresholds are defined:

Lower threshold (30): Indicates oversold conditions, triggering a potential buy.

Upper threshold (70): Indicates overbought conditions, prompting a possible sell.

Entry Conditions:

Buy Signal: The strategy initiates a buy order when the RSI crosses above the lower threshold (30), indicating a shift from oversold conditions.

Sell Signal: A sell order is triggered when the RSI crosses below the upper threshold (70), suggesting an overbought reversal.

Only one order (buy or sell) can be active at a time, ensuring that a new trade begins only when there’s no existing position.

Stop-Loss and Target Management:

For each trade, stop-loss and target conditions are applied to manage risk and secure profits.

For Buy Positions:

Stop-loss is set 100 points below the entry price.

Target is set 150 points above the entry price.

For Sell Positions:

Stop-loss is set 100 points above the entry price.

Target is 150 points below the entry price.

The strategy closes the trade when either the stop-loss or target is met, marking the trade as "closed" and allowing a new trade entry.

Trade Sequencing:

A new trade (buy or sell) is only permitted after the previous position hits either its stop-loss or target, preventing overlapping trades and ensuring clear trade sequences.

This sequential approach enhances risk management by ensuring only one active position at any time.

End-of-Day Closure:

All open positions are closed automatically at 3:25 PM (Indian market time) to avoid overnight exposure, ensuring the strategy remains strictly intraday.

The flag for trade entry is reset at the end of each day, enabling fresh trades the next day.

Chart Indicators:

The script plots buy and sell signals directly on the chart with visible labels.

It also displays the custom RSI metric with horizontal lines for the lower and upper thresholds, providing visual cues for entry and exit points.

Summary

This strategy is a momentum-based intraday trading approach that uses the RSI for identifying potential reversals and manages trades through predefined stop-loss and target levels. By enforcing trade sequencing and closing positions at the end of the trading day, it prioritizes risk management and seeks to capitalize on short-term trends while avoiding overnight market risks.

Simple RSI stock Strategy [1D] The "Simple RSI Stock Strategy " is designed to long-term traders. Strategy uses a daily time frame to capitalize on signals generated by the Relative Strength Index (RSI) and the Simple Moving Average (SMA). This strategy is suitable for low-leverage trading environments and focuses on identifying potential buy opportunities when the market is oversold, while incorporating strong risk management with both dynamic and static Stop Loss mechanisms.

This strategy is recommended for use with a relatively small amount of capital and is best applied by diversifying across multiple stocks in a strong uptrend, particularly in the S&P 500 stock market. It is specifically designed for equities, and may not perform well in other markets such as commodities, forex, or cryptocurrencies, where different market dynamics and volatility patterns apply.

Indicators Used in the Strategy:

1. RSI (Relative Strength Index):

- The RSI is a momentum oscillator used to identify overbought and oversold conditions in the market.

- This strategy enters long positions when the RSI drops below the oversold level (default: 30), indicating a potential buying opportunity.

- It focuses on oversold conditions but uses a filter (SMA 200) to ensure trades are only made in the context of an overall uptrend.

2. SMA 200 (Simple Moving Average):

- The 200-period SMA serves as a trend filter, ensuring that trades are only executed when the price is above the SMA, signaling a bullish market.

- This filter helps to avoid entering trades in a downtrend, thereby reducing the risk of holding positions in a declining market.

3. ATR (Average True Range):

- The ATR is used to measure market volatility and is instrumental in setting the Stop Loss.

- By multiplying the ATR value by a custom multiplier (default: 1.5), the strategy dynamically adjusts the Stop Loss level based on market volatility, allowing for flexibility in risk management.

How the Strategy Works:

Entry Signals:

The strategy opens long positions when RSI indicates that the market is oversold (below 30), and the price is above the 200-period SMA. This ensures that the strategy buys into potential market bottoms within the context of a long-term uptrend.

Take Profit Levels:

The strategy defines three distinct Take Profit (TP) levels:

TP 1: A 5% from the entry price.

TP 2: A 10% from the entry price.

TP 3: A 15% from the entry price.

As each TP level is reached, the strategy closes portions of the position to secure profits: 33% of the position is closed at TP 1, 66% at TP 2, and 100% at TP 3.

Visualizing Target Points:

The strategy provides visual feedback by plotting plotshapes at each Take Profit level (TP 1, TP 2, TP 3). This allows traders to easily see the target profit levels on the chart, making it easier to monitor and manage positions as they approach key profit-taking areas.

Stop Loss Mechanism:

The strategy uses a dual Stop Loss system to effectively manage risk:

ATR Trailing Stop: This dynamic Stop Loss adjusts based on the ATR value and trails the price as the position moves in the trader’s favor. If a price reversal occurs and the market begins to trend downward, the trailing stop closes the position, locking in gains or minimizing losses.

Basic Stop Loss: Additionally, a fixed Stop Loss is set at 25%, limiting potential losses. This basic Stop Loss serves as a safeguard, automatically closing the position if the price drops 25% from the entry point. This higher Stop Loss is designed specifically for low-leverage trading, allowing more room for market fluctuations without prematurely closing positions.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

Together, these mechanisms ensure that the strategy dynamically manages risk while offering robust protection against significant losses in case of sharp market downturns.

The position size has been estimated by me at 75% of the total capital. For optimal capital allocation, a recommended value based on the Kelly Criterion, which is calculated to be 59.13% of the total capital per trade, can also be considered.

Enjoy !

ICT Indicator with Paper TradingThe strategy implemented in the provided Pine Script is based on **ICT (Inner Circle Trader)** concepts, particularly focusing on **order blocks** to identify key levels for potential reversals or continuations in the market. Below is a detailed description of the strategy:

### 1. **Order Block Concept**

- **Order blocks** are price levels where large institutional orders accumulate, often leading to a reversal or continuation of price movement.

- In this strategy, **order blocks** are identified when:

- The high of the current bar crosses above the high of the previous bar (for bullish order blocks).

- The low of the current bar crosses below the low of the previous bar (for bearish order blocks).

### 2. **Buy and Sell Signal Generation**

The core of the strategy revolves around identifying the **breakout** of order blocks, which is interpreted as a signal to either enter or exit trades:

- **Buy Signal**:

- Generated when the closing price crosses **above** the last identified bullish order block (i.e., the highest point during the last upward crossover of highs).

- This signals a potential upward trend, and the strategy enters a long position.

- **Sell Signal**:

- Generated when the closing price crosses **below** the last identified bearish order block (i.e., the lowest point during the last downward crossover of lows).

- This signals a potential downward trend, and the strategy exits any open long positions.

### 3. **Strategy Execution**

The strategy is executed using the `strategy.entry()` and `strategy.close()` functions:

- **Enter Long Positions**: When a buy signal is generated, the strategy opens a long position (buying).

- **Exit Positions**: When a sell signal is generated, the strategy closes the long position.

### 4. **Visual Indicators on the Chart**

To make the strategy easier to follow visually, buy and sell signals are marked directly on the chart:

- **Buy signals** are indicated with a green upward-facing triangle above the bar where the signal occurred.

- **Sell signals** are indicated with a red downward-facing triangle below the bar where the signal occurred.

### 5. **Key Elements of the Strategy**

- **Trend Continuation and Reversals**: This strategy is attempting to capture trends based on the breakout of important price levels (order blocks). When the price breaks above or below a significant order block, it is expected that the market will continue in that direction.

- **Order Block Strength**: Order blocks are considered strong areas where price action could reverse or accelerate, based on how institutional investors place large orders.

### 6. **Paper Trading**

This script uses **paper trading** to simulate trades without actual money being involved. This allows users to backtest the strategy, seeing how it would have performed in historical market conditions.

### 7. **Basic Strategy Flow**

1. **Order Block Identification**: The script constantly monitors price movements to detect bullish and bearish order blocks.

2. **Buy Signal**: If the closing price crosses above the last order block high, the strategy interprets it as a sign of bullish momentum and enters a long position.

3. **Sell Signal**: If the closing price crosses below the last order block low, it signals a bearish momentum, and the strategy closes the long position.

4. **Visual Representation**: Buy and sell signals are displayed on the chart for easy identification.

### **Advantages of the Strategy:**

- **Simple and Clear Rules**: The strategy is based on clearly defined rules for identifying order blocks and trade signals.

- **Effective for Trend Following**: By focusing on breakouts of order blocks, this strategy attempts to capture strong trends in the market.

- **Visual Aids**: The plot of buy/sell signals helps traders to quickly see where trades would have been placed.

### **Limitations:**

- **No Shorting**: This strategy only enters long positions (buying). It does not account for shorting opportunities.

- **No Risk Management**: There are no built-in stop losses, trailing stops, or profit targets, which could expose the strategy to large losses during adverse market conditions.

- **Whipsaws in Range Markets**: The strategy could produce false signals in sideways or choppy markets, where breakouts are short-lived and prices quickly reverse.

### **Overall Strategy Objective:**

The goal of the strategy is to enter into long positions when the price breaks above a significant order block, and exit when it breaks below. The strategy is designed for trend-following, with the assumption that price will continue in the direction of the breakout.

Let me know if you'd like to enhance or modify this strategy further!

Intramarket Difference Index StrategyHi Traders !!

The IDI Strategy:

In layman’s terms this strategy compares two indicators across markets and exploits their differences.

note: it is best the two markets are correlated as then we know we are trading a short to long term deviation from both markets' general trend with the assumption both markets will trend again sometime in the future thereby exhausting our trading opportunity.

📍 Import Notes:

This Strategy calculates trade position size independently (i.e. risk per trade is controlled in the user inputs tab), this means that the ‘Order size’ input in the ‘Properties’ tab will have no effect on the strategy. Why ? because this allows us to define custom position size algorithms which we can use to improve our risk management and equity growth over time. Here we have the option to have fixed quantity or fixed percentage of equity ATR (Average True Range) based stops in addition to the turtle trading position size algorithm.

‘Pyramiding’ does not work for this strategy’, similar to the order size input togeling this input will have no effect on the strategy as the strategy explicitly defines the maximum order size to be 1.

This strategy is not perfect, and as of writing of this post I have not traded this algo.

Always take your time to backtests and debug the strategy.

🔷 The IDI Strategy:

By default this strategy pulls data from your current TV chart and then compares it to the base market, be default BINANCE:BTCUSD . The strategy pulls SMA and RSI data from either market (we call this the difference data), standardizes the data (solving the different unit problem across markets) such that it is comparable and then differentiates the data, calling the result of this transformation and difference the Intramarket Difference (ID). The formula for the the ID is

ID = market1_diff_data - market2_diff_data (1)

Where

market(i)_diff_data = diff_data / ATR(j)_market(i)^0.5,

where i = {1, 2} and j = the natural numbers excluding 0

Formula (1) interpretation is the following

When ID > 0: this means the current market outperforms the base market

When ID = 0: Markets are at long run equilibrium

When ID < 0: this means the current market underperforms the base market

To form the strategy we define one of two strategy type’s which are Trend and Mean Revesion respectively.

🔸 Trend Case:

Given the ‘‘Strategy Type’’ is equal to TREND we define a threshold for which if the ID crosses over we go long and if the ID crosses under the negative of the threshold we go short.

The motivating idea is that the ID is an indicator of the two symbols being out of sync, and given we know volatility clustering, momentum and mean reversion of anomalies to be a stylised fact of financial data we can construct a trading premise. Let's first talk more about this premise.

For some markets (cryptocurrency markets - synthetic symbols in TV) the stylised fact of momentum is true, this means that higher momentum is followed by higher momentum, and given we know momentum to be a vector quantity (with magnitude and direction) this momentum can be both positive and negative i.e. when the ID crosses above some threshold we make an assumption it will continue in that direction for some time before executing back to its long run equilibrium of 0 which is a reasonable assumption to make if the market are correlated. For example for the BTCUSD - ETHUSD pair, if the ID > +threshold (inputs for MA and RSI based ID thresholds are found under the ‘‘INTRAMARKET DIFFERENCE INDEX’’ group’), ETHUSD outperforms BTCUSD, we assume the momentum to continue so we go long ETHUSD.

In the standard case we would exit the market when the IDI returns to its long run equilibrium of 0 (for the positive case the ID may return to 0 because ETH’s difference data may have decreased or BTC’s difference data may have increased). However in this strategy we will not define this as our exit condition, why ?

This is because we want to ‘‘let our winners run’’, to achieve this we define a trailing Donchian Channel stop loss (along with a fixed ATR based stop as our volatility proxy). If we were too use the 0 exit the strategy may print a buy signal (ID > +threshold in the simple case, market regimes may be used), return to 0 and then print another buy signal, and this process can loop may times, this high trade frequency means we fail capture the entire market move lowering our profit, furthermore on lower time frames this high trade frequencies mean we pay more transaction costs (due to price slippage, commission and big-ask spread) which means less profit.

By capturing the sum of many momentum moves we are essentially following the trend hence the trend following strategy type.

Here we also print the IDI (with default strategy settings with the MA difference type), we can see that by letting our winners run we may catch many valid momentum moves, that results in a larger final pnl that if we would otherwise exit based on the equilibrium condition(Valid trades are denoted by solid green and red arrows respectively and all other valid trades which occur within the original signal are light green and red small arrows).

another example...

Note: if you would like to plot the IDI separately copy and paste the following code in a new Pine Script indicator template.

indicator("IDI")

// INTRAMARKET INDEX

var string g_idi = "intramarket diffirence index"

ui_index_1 = input.symbol("BINANCE:BTCUSD", title = "Base market", group = g_idi)

// ui_index_2 = input.symbol("BINANCE:ETHUSD", title = "Quote Market", group = g_idi)

type = input.string("MA", title = "Differrencing Series", options = , group = g_idi)

ui_ma_lkb = input.int(24, title = "lookback of ma and volatility scaling constant", group = g_idi)

ui_rsi_lkb = input.int(14, title = "Lookback of RSI", group = g_idi)

ui_atr_lkb = input.int(300, title = "ATR lookback - Normalising value", group = g_idi)

ui_ma_threshold = input.float(5, title = "Threshold of Upward/Downward Trend (MA)", group = g_idi)

ui_rsi_threshold = input.float(20, title = "Threshold of Upward/Downward Trend (RSI)", group = g_idi)

//>>+----------------------------------------------------------------+}

// CUSTOM FUNCTIONS |

//<<+----------------------------------------------------------------+{

// construct UDT (User defined type) containing the IDI (Intramarket Difference Index) source values

// UDT will hold many variables / functions grouped under the UDT

type functions

float Close // close price

float ma // ma of symbol

float rsi // rsi of the asset

float atr // atr of the asset

// the security data

getUDTdata(symbol, malookback, rsilookback, atrlookback) =>

indexHighTF = barstate.isrealtime ? 1 : 0

= request.security(symbol, timeframe = timeframe.period,

expression = [close , // Instentiate UDT variables

ta.sma(close, malookback) ,

ta.rsi(close, rsilookback) ,

ta.atr(atrlookback) ])

data = functions.new(close_, ma_, rsi_, atr_)

data

// Intramerket Difference Index

idi(type, symbol1, malookback, rsilookback, atrlookback, mathreshold, rsithreshold) =>

threshold = float(na)

index1 = getUDTdata(symbol1, malookback, rsilookback, atrlookback)

index2 = getUDTdata(syminfo.tickerid, malookback, rsilookback, atrlookback)

// declare difference variables for both base and quote symbols, conditional on which difference type is selected

var diffindex1 = 0.0, var diffindex2 = 0.0,

// declare Intramarket Difference Index based on series type, note

// if > 0, index 2 outpreforms index 1, buy index 2 (momentum based) until equalibrium

// if < 0, index 2 underpreforms index 1, sell index 1 (momentum based) until equalibrium

// for idi to be valid both series must be stationary and normalised so both series hae he same scale

intramarket_difference = 0.0

if type == "MA"

threshold := mathreshold

diffindex1 := (index1.Close - index1.ma) / math.pow(index1.atr*malookback, 0.5)

diffindex2 := (index2.Close - index2.ma) / math.pow(index2.atr*malookback, 0.5)

intramarket_difference := diffindex2 - diffindex1

else if type == "RSI"

threshold := rsilookback

diffindex1 := index1.rsi

diffindex2 := index2.rsi

intramarket_difference := diffindex2 - diffindex1

//>>+----------------------------------------------------------------+}

// STRATEGY FUNCTIONS CALLS |

//<<+----------------------------------------------------------------+{

// plot the intramarket difference

= idi(type,

ui_index_1,

ui_ma_lkb,

ui_rsi_lkb,

ui_atr_lkb,

ui_ma_threshold,

ui_rsi_threshold)

//>>+----------------------------------------------------------------+}

plot(intramarket_difference, color = color.orange)

hline(type == "MA" ? ui_ma_threshold : ui_rsi_threshold, color = color.green)

hline(type == "MA" ? -ui_ma_threshold : -ui_rsi_threshold, color = color.red)

hline(0)

Note it is possible that after printing a buy the strategy then prints many sell signals before returning to a buy, which again has the same implication (less profit. Potentially because we exit early only for price to continue upwards hence missing the larger "trend"). The image below showcases this cenario and again, by allowing our winner to run we may capture more profit (theoretically).

This should be clear...

🔸 Mean Reversion Case:

We stated prior that mean reversion of anomalies is an standerdies fact of financial data, how can we exploit this ?

We exploit this by normalizing the ID by applying the Ehlers fisher transformation. The transformed data is then assumed to be approximately normally distributed. To form the strategy we employ the same logic as for the z score, if the FT normalized ID > 2.5 (< -2.5) we buy (short). Our exit conditions remain unchanged (fixed ATR stop and trailing Donchian Trailing stop)

🔷 Position Sizing:

If ‘‘Fixed Risk From Initial Balance’’ is toggled true this means we risk a fixed percentage of our initial balance, if false we risk a fixed percentage of our equity (current balance).

Note we also employ a volatility adjusted position sizing formula, the turtle training method which is defined as follows.

Turtle position size = (1/ r * ATR * DV) * C

Where,

r = risk factor coefficient (default is 20)

ATR(j) = risk proxy, over j times steps

DV = Dollar Volatility, where DV = (1/Asset Price) * Capital at Risk

🔷 Risk Management:

Correct money management means we can limit risk and increase reward (theoretically). Here we employ

Max loss and gain per day

Max loss per trade

Max number of consecutive losing trades until trade skip

To read more see the tooltips (info circle).

🔷 Take Profit:

By defualt the script uses a Donchain Channel as a trailing stop and take profit, In addition to this the script defines a fixed ATR stop losses (by defualt, this covers cases where the DC range may be to wide making a fixed ATR stop usefull), ATR take profits however are defined but optional.

ATR SL and TP defined for all trades

🔷 Hurst Regime (Regime Filter):

The Hurst Exponent (H) aims to segment the market into three different states, Trending (H > 0.5), Random Geometric Brownian Motion (H = 0.5) and Mean Reverting / Contrarian (H < 0.5). In my interpretation this can be used as a trend filter that eliminates market noise.

We utilize the trending and mean reverting based states, as extra conditions required for valid trades for both strategy types respectively, in the process increasing our trade entry quality.

🔷 Example model Architecture:

Here is an example of one configuration of this strategy, combining all aspects discussed in this post.

Future Updates

- Automation integration (next update)

CCI and MACD Auto Trading Strategy with Risk/RewardOverview:

This strategy combines the Commodity Channel Index (CCI) and the Moving Average Convergence Divergence (MACD) indicators to automate trading decisions. It dynamically sets stop-loss and take-profit levels based on recent lows and highs, ensuring a risk/reward ratio of 1:1.5. This script aims to leverage trend and momentum signals while maintaining effective risk management.

Originality and Usefulness:

This script is not just a simple mashup of CCI and MACD indicators; it incorporates dynamic risk management by setting stop-loss and take-profit levels based on recent price action. This approach helps traders to:

・Identify potential trend reversals using the combination of CCI and MACD signals.

・Manage trades effectively by setting realistic stop-loss and take-profit levels based on recent market data.

・Maintain a balanced risk/reward ratio, which is essential for sustainable trading.

Indicators Used:

・CCI (Commodity Channel Index):

・Measures the deviation of the price from its average over a specified period, typically ranging from -100 to +100.

・Helps identify overbought and oversold conditions.

・MACD (Moving Average Convergence Divergence):

・Utilizes the difference between short-term and long-term moving averages to indicate trend strength and direction.

・Provides momentum signals that can be used for timing entries and exits.

How It Works:

Entry Conditions:

Long Entry:

・The MACD histogram is above zero.

・The CCI crosses above the -100 line.

Short Entry:

・The MACD histogram is below zero.

・The CCI crosses below the +100 line.

Exit Conditions:

Long Positions:

・The stop-loss is set at the recent low.

・The take-profit is set at 1.5 times the distance between the entry price and the stop-loss.

Short Positions:

・The stop-loss is set at the recent high.

・The take-profit is set at 1.5 times the distance between the entry price and the stop-loss.

Risk Management:

・The script dynamically adjusts stop-loss and take-profit levels based on recent market data, ensuring that the risk/reward ratio is maintained at 1:1.5.

・This approach helps in managing the risk effectively while aiming for consistent profits.

Strategy Properties:

・Account Size: Configured for a realistic account size suitable for the average trader.

・Commission and Slippage: Includes settings for realistic commission and slippage to reflect real market conditions.

・Risk per Trade: Designed to risk no more than 5-10% of equity per trade, aligning with sustainable trading practices.

・Backtesting Results: Configured to generate a sufficient sample size (ideally more than 100 trades) for reliable backtesting results.

Revised Backtesting Settings

Ensure that your backtesting settings are realistic:

・Account Size: Set a realistic initial capital suitable for the average trader.

・Commission and Slippage: Include realistic commission fees and slippage.

・Risk Management: Ensure that each trade risks no more than 5-10% of the account equity.

・Sufficient Sample Size: Choose a dataset that will generate more than 100 trades to provide a robust sample size.

BTC outperform atrategy### Code Description

This Pine Script™ code implements a simple trading strategy based on the relative prices of Bitcoin (BTC) on a weekly and a three-month basis. The script plots the weekly and three-month closing prices of Bitcoin on the chart and generates trading signals based on the comparison of these prices. The code can also be applied to Ethereum (ETH) with similar effectiveness.

### Explanation

1. **Inputs and Variables**:

- The user selects the trading symbol (default is "BINANCE:BTCUSDT").

- `weeklyPrice` retrieves the closing price of the selected symbol on a weekly interval.

- `monthlyPrice` retrieves the closing price of the selected symbol on a three-month interval.

2. **Plotting Data**:

- The weekly price is plotted in blue.

- The three-month price is plotted in red.

3. **Trading Conditions**:

- A long position is suggested if the weekly price is greater than the three-month price.

- A short position is suggested if the three-month price is greater than the weekly price.

4. **Strategy Execution**:

- If the long condition is met, the strategy enters a long position.

- If the short condition is met, the strategy enters a short position.

This script works equally well for Ethereum (ETH) by changing the symbol input to "BINANCE:ETHUSDT" or any other desired Ethereum trading pair.

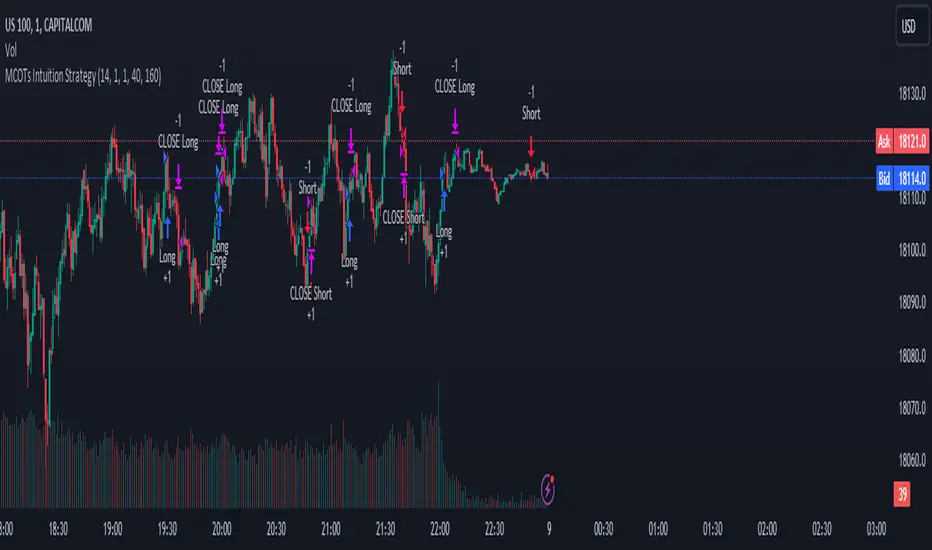

MCOTs Intuition StrategyInitial Capital: The strategy starts with an initial capital of $50,000.

Execution: Trades are executed on every price tick to capture all potential movements.

Contract Size: The default position size is one contract per trade.

Timeframe: Although not explicitly mentioned, this strategy is intended for a one-minute timeframe.

RSI Calculation: The Relative Strength Index (RSI) is calculated over a user-defined period (default is 14 periods).

Standard Deviation: The script calculates the standard deviation of the change in RSI values to determine the threshold for entering trades.

Exhaustion Detection: Before entering a long or short position, the script checks for exhaustion in the RSI’s momentum. This is to avoid entering trades during extreme conditions where a reversal is likely.

Entry Conditions: A long position is entered when the current RSI momentum exceeds the standard deviation threshold and is less than the previous momentum multiplied by an exhaustion factor. A short position is entered under the opposite conditions.

Limit Orders for Exit: Instead of traditional stop loss and take profit orders, the strategy uses limit orders to exit positions. This means the strategy sets a desired price level to close the position and waits for the market to reach this price.

Profit Target and Stop Loss: The script allows setting a profit target and stop loss in terms of ticks, which are the smallest measurable increments in price movement for the traded asset.

blah blah whatever

RSI Strategy with Manual TP and SL 19/03/2024This TradingView script implements a simple RSI (Relative Strength Index) strategy with manual take profit (TP) and stop-loss (SL) levels. Let's break down the script and analyze its components:

RSI Calculation: The script calculates the RSI using the specified length parameter. RSI is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and typically values above 70 indicate overbought conditions while values below 30 indicate oversold conditions.

Strategy Parameters:

length: Length of the RSI period.

overSold: Threshold for oversold condition.

overBought: Threshold for overbought condition.

trail_profit_pct: Percentage for trailing profit.

Entry Conditions:

For a long position: RSI crosses above 30 and the daily close is above 70% of the highest close in the last 50 bars.

For a short position: RSI crosses below 70 and the daily close is below 130% of the lowest close in the last 50 bars.

Entry Signals:

Long entry is signaled when both conditions for a long position are met.

Short entry is signaled when both conditions for a short position are met.

Manual TP and SL:

Take profit and stop-loss levels are calculated based on the entry price and the specified percentage.

For long positions, the take profit level is set above the entry price and the stop-loss level is set below the entry price.

For short positions, the take profit level is set below the entry price and the stop-loss level is set above the entry price.

Strategy Exits:

Exit conditions are defined for both long and short positions using the calculated take profit and stop-loss levels.

Chart Analysis:

This strategy aims to capitalize on short-term momentum shifts indicated by RSI crossings combined with daily price movements.

It utilizes manual TP and SL levels, providing traders with flexibility in managing their positions.

The strategy may perform well in ranging or oscillating markets where RSI signals are more reliable.

However, it may encounter challenges in trending markets where RSI can remain overbought or oversold for extended periods.

Traders should backtest this strategy thoroughly on historical data and consider optimizing parameters to suit different market conditions.

Risk management is crucial, so traders should carefully adjust TP and SL percentages based on their risk tolerance and market volatility.

Overall, this strategy provides a structured approach to trading based on RSI signals while allowing traders to customize their risk management. However, like any trading strategy, it should be used judiciously and in conjunction with other forms of analysis and risk management techniques.

TTP Intelligent AccumulatorThe intelligent accumulator is a proof of concept strategy. A hybrid between a recurring buy and TA-based entries and exits.

Distribute the amount of equity and add to your position as long as the TA condition is valid.

Use the exit TA condition to define your exit strategy.

Decide between adding only into losing positions to average down or take a riskier approach by allowing to add into a winning position as well.

Take full profit or distribute your exit into multiple take profit exists of the same size.

You can also decide if you allow your exit conditions to close your position in a loss or require a minimum take profit %.

The strategy includes a default built-in TA conditions just for showcasing the idea but the final intent of this script is to delegate the TA entries and exists to external sources.

The internal conditions use RSI length 7 crossing below the BB with std 1 for entries and above for exits.

To control the number of orders use the properties from settings:

- adjust the pyramiding

- adjust the percentage of equity

- make sure that pyramiding * % equity equals 100 to prevent over use of equity (unless using leverage)

The script is designed as an alternative to daily or weekly recurring buys but depending on the accuracy of your TA conditions it might prove profitable also in lower timeframes.

The reason the script is named Intelligent is because recurring buy is most commonly used without any decision making: buy no matter what with certain frequency. This strategy seeks to still perform recurring buys but filtering out some of the potential bad entries that can delay unnecessarily seeing the position in profits. The second reason is also securing an exit strategy from the beginning which no recurring buy option offers out-of-the-box.

Stx Monthly Trades ProfitMonthly profit displays profits in a grid and allows you to know the gain related to the investment during each month.

The profit could be computed in terms of gain/trade_cost or as percentage of equity update.

Settings:

- Profit: Monthly profit percentage or percentage of equity

- Table position

This strategy is intended only as a container for the code and for testing the script of the profit table.

Setting of strategy allows to select the test case for this snippet (percentage grid).

Money management: not relevant as strategy is a test case.

This script stand out as take in account the gain of each trade in relation to the capital invested in each trade. For example consider the following scenario:

Capital of 1000$ and we invest a fixed amount of 1000$ (I know is too risky but is a good example), we gain 10% every month.

After 10 months our capital is of 2000$ and our strategy is perfect as we have the same performance every month.

Instead, evaluating the percentage of equity we have 10% the first month, 9.9% the second (1200$/1100$ - 1) and 5.26% the tenth month. So seems that strategy degrade with times but this is not true.

For this reason, to evaluate my strategy I prefer to see the montly return of investment.

WARNING: The strategy provided with this script is only a test case and allows to see the behavior with different "trades" management, for these reason commision are set to zero.

At the moment only the provided test cases are handled:

test 1 - single entry and single exit;

test 2 - single entry and multiple exits;

test 3 - single entry and switch position;

hamster-bot MRS 2 (simplified version) MRS - Mean Reversion Strategy (Countertrend) (Envelope strategy)

This script does not claim to be unique and does not mislead anyone. Even the unattractive backtest result is attached. The source code is open. The idea has been described many times in various sources. But at the same time, their collection in one place provides unique opportunities.

Published by popular demand and for ease of use. so that users can track the development of the script and can offer their ideas in the comments. Otherwise, you have to communicate in several telegram chats.

Representative of the family of counter-trend strategies. The basis of the strategy is Mean reversion . You can also read about the Envelope strategy .

Mean reversion , or reversion to the mean, is a theory used in finance that suggests that asset price volatility and historical returns eventually will revert to the long-run mean or average level of the entire dataset.

The strategy is very simple. Has very few settings. Good for beginners to get acquainted with algorithmic trading. A simple adjustment will help avoid overfitting. There are many variations of this strategy, but for understanding it is better to start with this implementation.

Principle of operation.

1)

A conventional MA is being built. (fuchsia line). A limit order is placed on this line to close the position.

2)

(green line) A limit order is placed on this line to open a long position

3)

(red line) A limit order is placed on this line to open a short position

Attention!

Please note that a limit order is used. Conclude that the strategy has a limited capacity. And the results obtained on low-liquid instruments will be too high in the tester. On real auctions there will be a different result.

Note for testing the strategy in the spot market:

When testing in the spot market, do not include both long and short at the same time. It is recommended to test only the long mode on the spot. Short mode for more advanced users.

Settings:

Available types of moving averages:

SMA

EMA

TEMA - triple exponential moving average

DEMA - Double Exponential Moving Average

ZLEMA - Zero lag exponential moving average

WMA - weighted moving average

Hma - Hull Moving Average

Thma - Triple Exponential Hull Moving Average

Ehma - Exponential Hull Moving Average

H - MA built based on highs for n candles | ta.highest(len)

L - MA built based on lows for n candles | ta.lowest(len)

DMA - Donchian Moving Average

A Kalman filter can be applied to all MA

The peculiarity of the strategy is a large selection of MA and the possibility of shifting lines. You can set up a reverse trending strategy on the Donchian channel for example.

Use Long - enable/disable opening a Long position

Use Short - enable/disable opening a Short position

Lot Long, % - % allocated from the deposit for opening a Long position. In the spot market, do not use % greater than 100%

Lot Short, % - allocated % of the deposit for opening a Short position

Start date - the beginning of the testing period

End date - the end of the testing period (Example: only August 2020 can be tested)

Mul - multiplier. Used to offset lines. Example:

Mul = 0.99 is shift -1%

Mul = 1.01 is shift +1%

Non-strict recommendations:

1) Test the SPOT market on crypto exchanges. (The countertrend strategy has liquidation risk on futures)

2) Symbols altcoin/bitcoin or altcoin/altcoin. Example: ETH/BTC or DOGE/ETH

3) Timeframe is usually 1 hour

If the script passes moderation, I will supplement it by adding separate settings for closing long and short positions according to their MA

Vortex Cross w/MA ConfirmationThis script is a trading strategy that combines the Vortex Indicator and a Moving Average (MA) to generate potential entry signals for long and short positions.

1. Vortex Indicator:

The Vortex Indicator consists of two lines: Vortex Positive (VIP) and Vortex Negative (VIM). It is designed to identify trend direction and measure the strength of a trend.

2. Moving Average (MA):

The script uses a chosen type of Moving Average (SMA, EMA, SMMA, WMA, or VWMA) to smooth the price data. The smoothed line is referred to as the "Smoothing Line."

3. Determine Long and Short Conditions:

The script looks for potential long entry signals when VIP crosses above VIM, highlighting each crossover on the chart, and the closing price is above the Smoothing Line. It searches for short entry signals when VIM crosses above VIP, with the closing price is below the Smoothing Line. When the long or short conditions are met, the strategy enters either a long or short position accordingly.

Potential Usage:

The strategy can be utilized in trending markets, where the Vortex Indicator helps identify trend direction and strength, and the Moving Average smooths the price data to filter out some noise. It aims to capture trends and ride them while avoiding false signals during choppy or sideways markets.

BTFD strategy [3min]Hello

I would like to introduce a very simple strategy to buy lows and sell with minimal profit

This strategy works very well in the markets when there is no clear trend and in other words, the trend going sideways

this strategy works very well for stable financial markets like spx500, nasdaq100 and dow jones 30

two indicators were used to determine the best time to enter the market:

volume + rsi values

volume is usually the number of stocks or contracts traded over a certain period of time. Thus, it is an important indicator of market activity and liquidity. Each transaction constitutes an individual exchange between the buyer and the seller and constitutes the trading volume of a given instrument or asset.

The RSI measures the strength of uptrends versus downtrends. The signal is the entry or exit of the indicator value of the oversold or overbought level of the market. It is assumed that a value below or equal 30 indicates an oversold level of the market, and an RSI value above or equal 70 indicates an overbought level.

the strategy uses a maximum of 5 market entries after each candle that meets the condition

uses 5 target point levels to close the position:

tp1= 0.4%

tp2= 0.6%

tp3= 0.8%

tp4= 1.0%

tp5= 1.2%

after reaching a given profit value, a piece of the position is cut off gradually, where tp5 closes 100% of the remaining position

each time you enter a position, a stop loss of 5.0% is set, which is quite a high value, however, when buying each, sometimes very active downward price movement, you need a lot of space for market decisions in which direction it wants to go

to determine the level of stop loss and target point I used a piece of code by RafaelZioni , here is the script from which a piece of code was taken

this strategy is used for automation, however, I would recommend brokers that have the lowest commission values when opening and closing positions, because the strategy generates very high commission costs

Enjoy and trade safe ;)

D-BoT Alpha 'Short' SMA and RSI StrategyDostlar selamlar,

İşte son derece basit ama etkili ve hızlı, HTF de çok iyi sonuçlar veren bir strateji daha, hepinize bol kazançlar dilerim ...

Nedir, Nasıl Çalışır:

Strateji, iki ana girdiye dayanır: SMA ve RSI. SMA hesaplama aralığı 200 olarak, RSI ise 14 olarak ayarlanmıştır. Bu değerler, kullanıcı tercihlerine veya geriye dönük test sonuçlarına göre ayarlanabilir.

Strateji, iki koşul karşılandığında bir short sinyali oluşturur: RSI değeri, belirlenen bir giriş seviyesini (burada 51 olarak belirlenmiş) aşar ve kapanış fiyatı SMA değerinin altındadır.

Strateji, kısa pozisyonu üç durumda kapatır: Kapanış fiyatı, takip eden durdurma seviyesinden (pozisyon açıldığından beri en düşük kapanış olarak belirlenmiştir) büyükse, RSI değeri belirlenen bir durdurma seviyesini (bu durumda 54) aşarsa veya RSI değeri belirli bir kar al seviyesinin (bu durumda 32) altına düşerse.

Güçlü Yönleri:

İki farklı gösterge (SMA ve RSI) kullanımı, yalnızca birini kullanmaktan daha sağlam bir sinyal sağlayabilir.

Strateji, karları korumaya ve fiyat dalgalanmalarında kayıpları sınırlamaya yardımcı olabilecek bir iz süren durdurma seviyesi içerir.

Script oldukça anlaşılır ve değiştirmesi nispeten kolaydır.

Zayıf Yönleri:

Strateji, hacim, oynaklık veya daha geniş piyasa eğilimleri gibi diğer potansiyel önemli faktörleri göz önünde bulundurmaz.

RSI seviyeleri ve SMA süresi için belirli parametreler sabittir ve tüm piyasa koşulları veya zaman aralıkları için optimal olmayabilir.

Strateji oldukça basittir. Trade maliyetini (kayma veya komisyonlar gibi) hesaba katmaz, bu da trade performansını önemli ölçüde etkileyebilir.

Bu Stratejiyle Nasıl İşlem Yapılır:

Strateji, short işlemler için tasarlanmıştır. RSI, 51'in üzerine çıktığında ve kapanış fiyatı 200 periyotluk SMA'nın altında olduğunda işleme girer. RSI, 54'ün üzerine çıktığında veya 32'nin altına düştüğünde veya fiyat, pozisyon açıldığından beri en düşük kapanış fiyatının üzerine çıktığında işlemi kapatır.

Lütfen Dikkat, bu strateji veya herhangi bir strateji izole bir şekilde kullanılmamalıdır. Tüm bu çalışmalar eğitsel amaçlıdır. Yatırım tavsiyesi içermez.

This script defines a trading strategy based on Simple Moving Average (SMA) and the Relative Strength Index (RSI) indicators. Here's an overview of how it works, along with its strengths and weaknesses, and how to trade using this strategy:

How it works:

The strategy involves two key inputs: SMA and RSI. The SMA length is set to 200, and the RSI length is set to 14. These values can be adjusted based on user preferences or back-testing results.

The strategy generates a short signal when two conditions are met: The RSI value crosses over a defined entry level (set at 51 here), and the closing price is below the SMA value.

When a short signal is generated, the strategy opens a short position.

The strategy closes the short position under three conditions: If the close price is greater than the trailing stop (which is set as the lowest close since the position opened), if the RSI value exceeds a defined stop level (54 in this case), or if the RSI value drops below a certain take-profit level (32 in this case).

Strengths:

The use of two different indicators (SMA and RSI) can provide a more robust signal than using just one.

The strategy includes a trailing stop, which can help to protect profits and limit losses as the price fluctuates.

The script is straightforward and relatively easy to understand and modify.

Weaknesses:

The strategy doesn't consider other potentially important factors, such as volume, volatility, or broader market trends.

The specific parameters for the RSI levels and SMA length are hard-coded, and may not be optimal for all market conditions or timeframes.

The strategy is very simplistic. It doesn't take into account the cost of trading (like slippage or commissions), which can significantly impact trading performance.

How to trade with this strategy:

The strategy is designed for short trades. It enters a trade when the RSI crosses above 51 and the closing price is below the 200-period SMA. It will exit the trade when the RSI goes above 54 or falls below 32, or when the price rises above the lowest closing price since the position was opened.

Please note, this strategy or any strategy should not be used in isolation. It's important to consider other aspects of trading such as risk management, capital allocation, and combining different strategies to diversify. Back-testing the strategy on historical data and demo trading before going live is also a recommended practice.

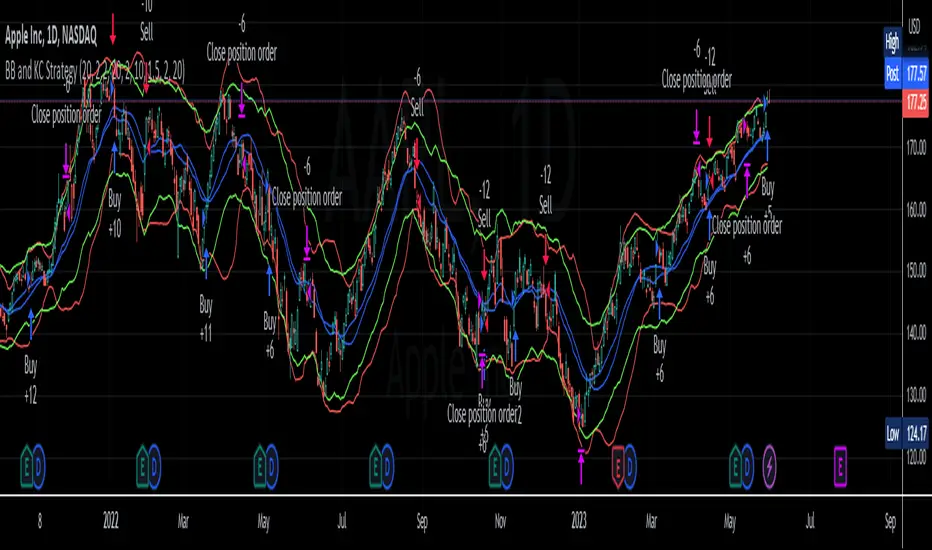

BB and KC StrategyThis script is designed as a TradingView strategy that uses Bollinger Bands (BB) and Keltner Channels (KC) as the primary indicators for generating trade signals. It aims to catch potential market trends by comparing the movements of these two popular volatility measures.

Key aspects of this strategy:

1. **Bollinger Bands and Keltner Channels:** Both are volatility-based indicators. The Bollinger Bands consist of a middle band (simple moving average) and two outer bands calculated based on standard deviation, which adjusts itself to market conditions. Keltner Channels are a set of bands placed above and below an exponential moving average of the price. The distance between the bands is calculated based on the Average True Range (ATR), a measure of price volatility.

2. **Entry Signals:** The strategy enters a long position when the upper KC line crosses above the upper BB line and the volume is above its moving average. Conversely, it enters a short position when the lower KC line crosses below the lower BB line and the volume is above its moving average.

3. **Exit Signals:** The strategy exits a position under two conditions. First, if the trade has been open for a certain number of bars defined by the user (default 20 bars). Second, a stop loss and trailing stop are in place to limit potential losses and lock in profits as the price moves favorably. The stop loss is set at a percentage of the entry price (default 1.5% for long and -1.5% for short), and the trailing stop is also a percentage of the entry price (default 2%).

4. **Trade Quantity:** The script allows specifying the investment amount for each trade, set to a default of 1000 currency units.

Remember, this is a strategy script, which means it is used for backtesting and not for real-time signals or live trading. It is also recommended that it is used as a tool to aid your trading, not as a standalone system. As with any strategy, it should be tested over different market conditions and used in conjunction with other aspects of technical and fundamental analysis to ensure robustness and effectiveness.

Volatility Breakout Strategy [Angel Algo]As traders, we're always looking for opportunities to profit from sudden price breakouts, and the Volatility Breakout Strategy aims to do just that.

This script is the perfect starting point for traders who want to experiment with capturing price movements resulting from increased volatility. The script plots the Average True Range (ATR) on the chart, which is a measure of the asset's volatility over a specified period. By setting the "Length" parameter, you can customize the period over which the volatility is measured.

Using the ATR, the strategy calculates upper and lower breakout levels and plots them on the chart. The signals for long and short positions are generated when the price crosses above the upper breakout level or below the lower breakout level, respectively. They are confirmed by checking the current bar state.

The strategy also fills the space between the upper and lower breakout levels with a color that indicates the latest signal direction. This feature helps traders quickly identify the prevailing trend.

The strategy uses the generated signals to enter trades. When a long or short signal is confirmed, and there is no open position in the direction of the signal, the strategy enters a long or short trade, respectively.

Choice of parameters.

Choosing the right value for the Length input parameter is crucial for tailoring the Volatility Breakout Strategy to suit your trading preferences. In general, a higher Length value implies a focus on capturing longer price moves. For instance, in this script, we have set the Length value to 20, resulting in trades that span approximately 100 candles. These trades encompass price trends consisting of multiple swings.

However, if your goal is to trade individual swings rather than longer trends, it's advisable to experiment with smaller values for the Length parameter. By reducing the Length, you can target shorter-term price movements and potentially increase the frequency of trades.

It's important to note that while a higher Length value tends to lead to longer trades, there is no strict correlation between the Length parameter and the average length of trades. This can vary across different markets. Therefore, it's essential to conduct thorough experimentation with various Length values and closely observe the length of trades they generate. Comparing these trade lengths with the average trend or swing length in the specific market can provide valuable insights.

Ideally, you should aim to select a Length value that aligns with the average trend or swing length observed in the market you are trading. This way, you can optimize the strategy to capture price movements that closely match the prevailing market conditions.

Remember, finding the optimal Length value is a process of trial and error, combined with careful observation of trade lengths and their correlation with market trends. So, don't be afraid to experiment and refine the Length parameter to maximize the effectiveness of the Volatility Breakout Strategy in your chosen market.

Disclaimer: This trading strategy is provided for educational and informational purposes only.Trading involves risk, and past performance is not indicative of future results.

DCA Simulator A simple yet powerful Dollar Cost Averaging (DCA) simulator.

You just add the script to your chart, and you'll be able to see:

- Every single entry with its size

- The evolution of you average price in time (blue line)

- The profit and loss areas (where market price < average price the DCA is at loss, and the background is colored in red. At the contrary, where mkt price is > average price, it's profit area and the background is green).

- Max drawdown: the point in price and time where the DCA loss is maximum in the considered time interval. The drawdown amount is specified.

- Profit (or loss) and total cost at the end of the time interval or at the present day: the script shows how much the DCA is netting at a profit or loss, as well as the total cost of the DCA itself.

The parameters are:

- Date start and date end: time interval of the DCA simulation

- DCA period (you can choose between daily, weekly and monthly)

- Week day or month day if you choose those periods

- Single operation size (in base currency)

- Option to choose a DCA LONG or DCA SHORT (for uber bears)

- Option to include an exit strategy that partially closes your position (the % size closed can be chosen as well with the parameter "exit_close_perc") every time the DCA realizes a specific gain (choosable with the parameter "exit_gain_threshold"). If you choose "none" as an exit strategy, the script will assume to never close positions until the end of the period or the present day for simulation purpose.

NB: just ignore the TV strategy tester results, all the data are visible on the chart.

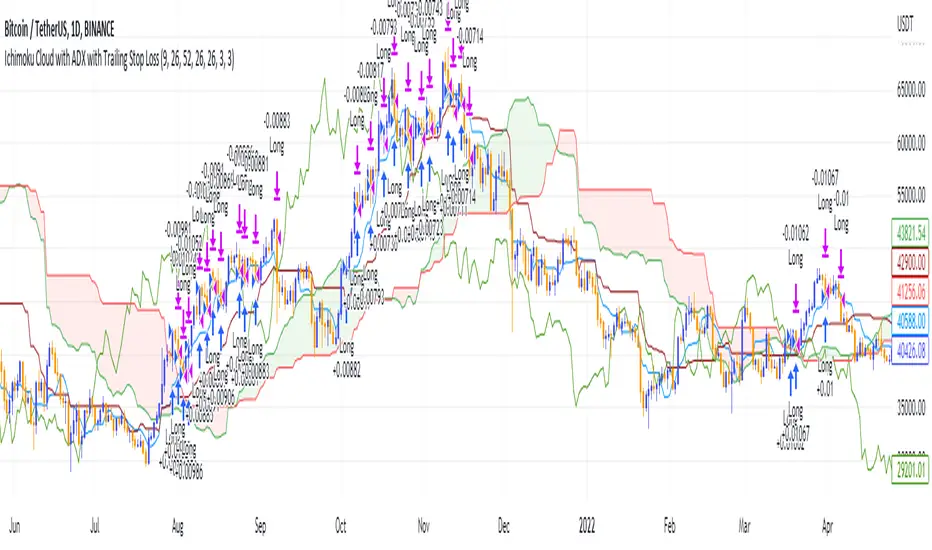

Ichimoku Cloud and ADX with Trailing Stop Loss (by Coinrule)The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on a chart. It also uses these figures to compute a “cloud” that attempts to forecast where the price may find support or resistance in the future.

The Ichimoku Cloud was developed by Goichi Hosoda, a Japanese journalist, and published in the late 1960s. It provides more data points than the standard candlestick chart. While it seems complicated at first glance, those familiar with how to read the charts often find it easy to understand with well-defined trading signals.

The Ichimoku Cloud is composed of five lines or calculations, two of which comprise a cloud where the difference between the two lines is shaded in.

The lines include a nine-period average, a 26-period average, an average of those two averages, a 52-period average, and a lagging closing price line.

The cloud is a key part of the indicator. When the price is below the cloud, the trend is down. When the price is above the cloud, the trend is up.

The above trend signals are strengthened if the cloud is moving in the same direction as the price. For example, during an uptrend, the top of the cloud is moving up, or during a downtrend, the bottom of the cloud is moving down.

DMI is simple to interpret. When +DI > - DI, it means the price is trending up. On the other hand, when -DI > +DI , the trend is weak or moving on the downside. The ADX does not give an indication about the direction but about the strength of the trend.

Typically values of ADX above 25 mean that the trend is steeply moving up or down, based on the -DI and +D positioning. This script aims to capture swings in the DMI, and thus, in the trend of the asset, using a contrarian approach.

Trading on high values of ADX, the strategy tries to spot extremely oversold and overbought conditions. Values of ADX above 45 may suggest that the trend has overextended and is may be about to reverse.

This strategy combines the Ichimoku Cloud with the ADX indicator to better enter trades.

Long orders are placed when these basic signals are triggered.

Long Position:

Tenkan-Sen is above the Kijun-Sen

Chikou-Span is above the close of 26 bars ago

Close is above the Kumo Cloud

MACD line crosses over the signal line

-DI is greater than +DI

ADX is greater than 45

Close Position:

3% increase trailing

3% decrease trailing

The script is backtested from 1 January 2018 and provides good returns.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

This script also works well on MATIC (1d timeframe), ETH (1d timeframe), and SOL (1d timeframe).

[XRP][1h] Chanu Delta inspired — Breakeven StrategyHello, this is my first TV contribution. I usually don't publish anything but the script is a quick review of an other contributor (Chanu Delta V3 script )

I reverse engineered this indicator today as I wanted to test it on other contracts. The original version (which aims to be traded on BTC) has been ported to XRP (as btc and xrp prices are narrowly correlated) then modified with a couple of what I believe are improvements:

- No backtest bias even with `security` function.

- Extra backtest bias validation, always trading on next bar as Crossover/under bias is confirmed

- Backtest with 2 ajustable TP, ajustable equity and breakeven option

- The current version is not design to use pyramiding as it would require extra logic to monitor the lifecycle of the position in the context of a study.

- Commented alerts examples with variables available in script scope so you can use them in alerts (just replace strategy with indicator and remove backtest related code block).

- Trade filling assumption set to 10, fees to 0.02 as the are default bybit maker fees and I advice to enter with trailing orders using a max of 2 ticks as offset to lower fees rather than a market order!

- Backtest and Alerts happen on barclose.

- No repaint guaranteed.

There are a thousand ways to improve it (adx/bb based dynamic TP/SL, order lifecycle, pyramiding...) but it seems to be a cool starting point.

Don't forget to have fun!